Price Dynamics

In this chapter, we develop mathematical models to study the dynamics of asset prices over time. We begin with simple concepts of interests in discrete time capturing the time value of money. We then update the model to continuous time framework where an ordinary differential equation is obtained to describe the evolution of the deterministic price value under constant interest rate, ignoring the randomness. Finally, we extend the framework to stochastic models, where uncertainty in price movements is incorporated through a Wiener process. We also list some of the commonly used stochastic differential equations for stock prices and interest rates, which form the foundation of modern quantitative finance.

Deterministic Interest-rate Models

The interest, expressed as a percentage divided by 100, is referred to as the interest rate.

Typically, interest rates are calculated annually. In this section, we explore the theory of interest rates using a bank fixed deposit as an example of an investment tool. These concepts can be easily applied to other types of investment tools.

Let \(t\) denote the time variable. We consider \(t=0\) as the initial time of investment, and the investment period spans the interval \([0, T]\), where \(T > 0\) denotes the maturity time. The interest is paid at a certain frequency, representing the number of times interest is paid per annum. For example, if the interest is paid quarterly, the frequency is 4.

If the frequency of interest payments is denoted by \(m\), with \(n=mT\) being an integer, then the times at which interest payments are due are given by

Let \(r\) denote the interest rate per annum (or annual interest rate), expressed as a decimal (i.e., \(r \times 100%\)). In this case, each interest payment is calculated at the rate \(r/m\), which is referred to as the per period rate.

Discrete Time Models

Let the principal be denoted by \(P(0)\) and the interest rate be \(r\) per annum. Let the payout frequency be \(m\) and the maturity time be \(T\), with \(n=mT\) being an integer. Let us derive the formula for compound interest.

At time \(t=t_1\), the accumulated amount is

which is considered as the principal for the period \((t_1,t_2].\)

At time \(t=t_2\), we have

Continuing in this way, we see that

In particular, at the maturity \(T\), the net amount obtained by the creditor (equivalently, the net amount paid by the debtor) is given by

which is the nominal value or the future value of the investment with compound interest. The factor \(\left(1+\frac{r}{m}\right)^{n}\) is called the growth factor for compound interest.

Observe that the compound interest scheme is significantly influenced by the payout frequency \(m\). As the frequency increases, the maturity amount in the compound interest scheme also increases.

Mr. Megh invests ₹ 100 in a bank fixed deposit scheme at the rate of 10% per annum and for two and a half years. Assume that the bank pays out the interest every quarter. Then, the interest is paid 10 times to Mr. Megh with the interest payout frequency 4. Hence, we have \(m=4,\) whereas \(T=2.5,\) \(P(0)=100,\) and \(r=0.1\).

Using the compound interest formula, we can determine the accumulated amount at maturity (the nominal value), given by

Let us now increase the payout frequency from every quarter to every month, then we have \(m=12\) (instead of \(m=4\)) and the nominal value of the investment becomes

Hence the total interest obtained is ₹ 28.27, which is higher than the interest obtained with the quarterly compounding scheme.

Since \(n=mT\), the above expression can be rewritten as

Using this formula, we can find the EAR in the above example as \(r_e \approx 0.1038\) (or 10.38%).

The basic annual interest rate (\(r=0.1\) in the above example) is termed the nominal annual rate (NAR) or simply the interest rate per annum or nominal interest rate.

- 3% compounded monthly for one year.

- 18% compounded quarterly for one year.

Continuous Time Model

The compound interest discussed above assumes discrete payout times with a finite payout frequency \(m\). However, in theoretical contexts, it is often necessary to model compounding in a continuous time framework, which can be achieved by taking \(m\rightarrow \infty\). This is equivalent to taking \(n\rightarrow \infty\) in (2.1) and leads to

the nominal value (or the future value) of the investment under continuous compound interest.

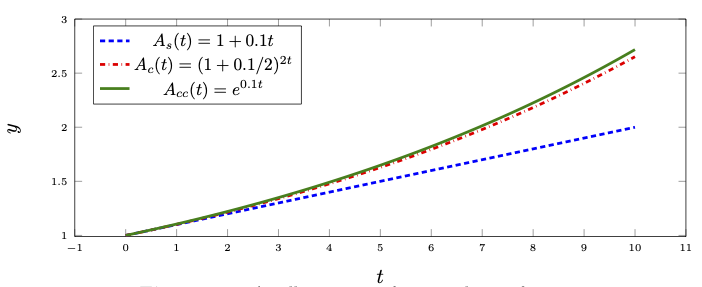

The factors

are referred to as the accumulation factor for simple interest, compound interest, and continuous compound interest, respectively. The following figure illustrates the behavior of these three accumulation factors over time.

\(~\)

Often practitioners prefer continuous compounding interest rate in their models rather than discrete compounding interest rate. This may be because different markets often have different day count conventions. The following problem provides formulae to convert one interest rate to the other.

Non-constant Interest Rate

We have derived the formula for continuous compounding in the case of a constant interest rate. However, a more realistic situation involves considering an interest rate that changes continuously over time. Hence, we need a model to calculate \(P(t)\) for all \(t \in [0,T]\), where \(r=r(t)\) represents the time-dependent interest rate.

We now derive an ODE that models the continuous compounding scheme with interest rate \(r=r(t)\) per annum at any given time \(t\in [0,T]\).

For a given number \(\Delta t>0\), the net interest obtain for the period \([t,t+\Delta t]\) is given by \(P(t+\Delta t) - P(t)\), for any \(t\in [0,T-\Delta t]\). Assume that \(\Delta t\) is very small so that the compound interest during the period \([t,t+\Delta t]\) is approximately the same as the simple interest. In other words, we take

Dividing both sides by \(\Delta t\) and then letting \(\Delta t\rightarrow 0\), we get

This leads to the required model, which is an ordinary differential equation (ODE) given by

If we assume the interest rate \(r\) to be a constant, then the solution of (2.4) at \(t=T\), with the initial condition as the principal \(P(0)\), is given by (2.2).

Integrating (2.4) over \([0,t]\), we can derive our required model as the integral equation

Using the fundamental theorem of calculus, we can see that if \(r\) and \(P\) are continuous, then (2.4) and (2.5) are equivalent.

where the principle value \(P(0)\) is given.

Another important random phenomenon in finance is the mean-reverting process. Many natural and economic systems exhibit a mean-reverting tendency of a state variable (for instance, an interest rate), which can be described as follows:

Whenever the state variable deviates significantly from its long-term equilibrium (mean) level, forces arise that drive it back toward that mean.

Show that the solution of the ODE

is

By taking \(r(t)=r_t\), obtain the particular solution of the ODE (2.4) at some time \(T>0\).

The above problem shows the deterministic part of such dynamics and highlights the role of the stochastic part of mean-reverting models, which will be introduced at a later part of this chapter.

Present Value

So far, we have established models to calculate the nominal value \(P(T)\) of a deposit, given the principal \(P(0)\), interest rate \(r\), and the frequency \(m\) of the interest payment per year. Here \(P(T)\) can be regarded as the future value of the principal \(P(0)\) with respect to the given interest rate \(r\) and the frequency \(m\).

The concept of present value is the inverse of future value, where \(P(T)\) is given, and we are required to find \(P(0)\) for the given values of \(r\) and \(m\).

The present value with simple interest is given by

In the case of a compound interest scheme, the present value is given by

where \(m\) denotes the frequency (the number of times interest is accumulated per annum) and \(n=mT\) is the total number of times interest is accumulated during the entire investment period.

Finally, for a continuous compounding scheme, the present value is given by

The procedure of finding the present value for a future amount is referred to as discounting. Correspondingly, the present value is often referred to as discount value. The factor by which the present value \(P(0)\) is discounted from the future value \(P(T)\) is called the discount factor. The discount factor for simple interest, compound interest, and continuous compound interest are, respectively,

Cash Flow Stream

The concepts of present and future values can be extended to a sequence of cash flows occurring at multiple times. Let us first introduce the concept of a cash flow stream.

For a given time partition \(\{t_0,t_1,\ldots,t_n\}\) of the period \([0,T]\) with \(0=t_0 < t_1

Whenever the time partition is important, we may also represent a cash flow stream as (\(\boldsymbol{x},\boldsymbol{t}\)), where \(\boldsymbol{t} = (t_0,t_1,\ldots,t_n)\).

The future value of a cash flow stream \(\boldsymbol{x} = (x_0,x_1,\ldots,x_n)\) at the rate of \(r\) (per annum) during the time period \([0,T]\) with equally spaced time partition \(\{t_0,t_1,\ldots, t_n\}\) (with \(t_0=0\) and \(t_n=T\)) is given by

We can see that \(\tilde{r}\) represents the interest rate per period. Using \(\tilde{r}\) in the discrete compound interest formula, we get

Answer: \(\boldsymbol{x}=(1000,1000,\ldots,1000, -12397.24)\)

We now discuss the present value of a cash flow stream. Consider a cash flow stream \(\boldsymbol{x} = (x_0,x_1,\ldots,x_n)\). The present value of the cash flow stream \(\boldsymbol{x}\) at the interest rate of \(r\) per annum and for the time period \([0,T]\) with equally spaced time partition \(\{t_0,t_1,\ldots, t_n\}\) (with \(t_0=0\) and \(t_n=T\)) is given by

where \(D_k\) denotes the discount factor at time \(t_k\) given by one of the formulae in (2.6) (with \(n=mT\)) depending on the type of the interest scheme. More precisely, we have

\(~\)

One can use present value to compare investments and prefer the one that yields higher value.

The corresponding cash flow streams are

If the prevailing interest rate is 6% per annum compounded annually, then which of the two cash flow streams is preferable?

To answer this question, let's calculate the net present value (NPV) for both streams. We have

Therefore, based on the NPV criterion, it is more profitable to sell the goats at the end of the first year.

Answer the following questions with annual compound interest rates:

- If \(r = 4.5%\), which cash flow is more profitable?

- If \(r = 9%\), which cash flow is more profitable?

Often it is useful to consider an uncountable cash flow stream defined by a function \(f(t)\). The future value of such a cash flow stream under a constant interest rate \(r\) is given by

and the present value is given by

The following example illustrates a potential application of a continuous cash flow stream and its present value.

Stochastic Models

Deterministic models discussed in the previous section captures the average or expected growth of financial variables such as prices or interest rates. However, real-world financial markets are inherently noisy and uncertain, and these variables are influenced by unpredictable factors such as news events, macroeconomic shocks, investor sentiments, and market reactions. Consequently, their dynamics cannot be modeled deterministically and to account this randomness, we extend our framework to include stochastic components, leading to stochastic differential equations (SDEs).

Stochastic Processes

In this subsection, we denote a financial variable by \(X\) (from our previous discussions, \(X\) can be the principal \(P\) or interest-rate \(r\)). In deterministic setup, \(X\) is viewed as a deterministic function of time \(X=X(t)\), where each time \(t\) corresponds to a single predictable value. However, in stochastic modeling, we abandon this deterministic view and treat \(X\) as a stochastic process.

Let \(\mathbb{T}\) denote the time index set. A collection of random variables \(\{X_t~|~t\in \mathbb{T}\}\) defined on a probability space \((\Omega, \mathcal{F}, \mathbb{P})\) is called a stochastic process. If \(\mathbb{T}\) is an interval, then \(\{X_t\}\) is a continuous-time stochastic process and if \(\mathbb{T}\) is finite or countably infinite, then the process is a discrete-time stochastic process.

- For a fixed time \(t\in \mathbb{T}\), \(X_t:\Omega\rightarrow \mathbb{R}\) is a random variable and we write

\[ X(\omega) = X_t(\omega), ~ \omega\in \Omega. \]

- For a fixed random outcome \(\omega\in \Omega\), \(X:\mathbb{T}\rightarrow \mathbb{R}\) is a (deterministic) function of time,

\[ X(t) = X_t(\omega), ~t\in \mathcal{T}, \]

called a sample path of the process.

The time evolution of financial quantities inherently involve randomness, where the information unfolds progressively as events occur. This gradual flow of information is represented mathematically by the concept of filtration.

A collection \(\{\mathcal{F}_t~|~t\in \mathbb{T}\}\) of \(\sigma\)-fields on a sample space \((\Omega,\mathcal{F})\) is called a filtration if

A probability space \((\Omega,\mathcal{F},\mathbb{P}, \{\mathcal{F}_t\})\) is called a filtered probability space.

In a finite horizon \([0, T]\) with partition \(\mathbb{T}_n = \{0=t_0, t_1, \ldots, t_n=T\}\), we often consider a filtration \(\{\mathcal{F}_k~|~k=0,1,\ldots, n\}\) with \(\mathcal{F}_n = \mathcal{F},\) the \(\sigma\)-field of the probability space (as obtained in Example «Click Here» ).

Often, filtrations are constructed using generated \(\sigma\)-fields, either from a partition of \(\Omega\) or from a stochastic process. These are the natural filtrations in financial applications. Here, we recall the definition of a generated \(\sigma\)-field by a partition of \(\Omega\) and postpone the discussion of \(\sigma\)-field generated by stochastic processes to a later chapter.

For a given collection of subsets \(\{E_1, E_2, \ldots \}\) (finite or infinite) of \(\Omega\), the generated \(\sigma\)-field, denoted by \(\sigma\{E_1, E_2, \ldots \}\), is defined as the intersection of all \(\sigma\)-fields on \(\Omega\) that contain the given collection. Equivalently, it is the smallest \(\sigma\)-field containing \(\{E_1, E_2, \ldots\}\).

Let us recall an elementary result from probability.

The following lemma is a direct consequence of the above problem.

Each \(\sigma\)-field \(\mathcal{F}_t\) in a filtration can be interpreted as the collection of all information (about the market or a particular stock) that is available to an investor at time \(t\). This idea is illustrated in the following example.

Given a pair of real numbers \(0 < B < 1 < U\). Consider a set of discrete time points \(\mathbb{T} = \{t_0, t_1, t_2\}\) and a sample space

where each \(\omega=m_1m_2 \in \Omega\), with \(m_1,m_2\in \{U,D\}\), represents a possible sequence of a stock price movements at two time levels \(t_1\) and \(t_2,\) where U stands for an upward move and D represents a downward move.

Let us now choose a filtration that is relevant for the present problem.

The information available at \(t_1\) is then represented by the generated \(\sigma\)-field of the partition \(\{E_1, E_2\}\) of \(\Omega\). That is,

of \(\Omega\). That is,

Thus, the collection of \(\sigma\)-fields \(\{\mathcal{F}_0, \mathcal{F}_1, \mathcal{F}_2\}\) defined on \(\Omega\) satisfies the condition

and hence forms a filtration on the sample space \((\Omega, 2^\Omega)\). We refer to this filtration as the natural filtration for the binomial stock price process in discrete-time setup. This filtration represents the gradual flow of information over time, where as time progresses, the investor learns more about the realized path of the stock price.

The information structure described by a filtration is that the information increases in time and at any fixed time \(t\) an investor knows all information from the past to present but has no knowledge of future events. In financial terms, this expresses the no-insider-trading assumption: decisions at time \(t\) can depend only on currently available information.

In stochastic modeling, it is essential that the random quantities we study (such as stock prices, interest rates, or portfolio values) evolve consistently with the flow of information represented by the filtration. This needs another important concept called the adapted process.

A stochastic process \(\{X_t~|~t\in \mathbb{T}\}\) defined on a probability space \((\Omega, \mathcal{F},\mathbb{P})\) is said to be adapted to a filtration \(\{\mathcal{F}_t~|~t\in \mathbb{T}\}\) if \(X_t\) is \(\mathcal{F}_t\)-measurable, for every \(t\in \mathbb{T}\).

From the above definition, we see that an adapted process represents a realistic financial quantity whose evolution respects the market’s information structure.

Let the initial stock price \(S_0>0\) at time \(t_0\) (present time) be known, and let the up and down factors be \(U=1.1\) and \(D=0.95\), respectively. For \(\mathbb{T} = \{t_0,t_1, t_2\}\), with \(t_1 < t_2\), consider the sample space \((\Omega, 2^\Omega)\), where \(\Omega\) is given in Example «Click Here» with \(UD = U\times D.\)

Let us use the notation \(\omega = m_1\times m_2\), for any \(\omega \in \Omega\), where each \(m_1, m_2\in \{U,D\}\). Define the stochastic process \(S = \{S_k~|~ t_k \in \mathbb{T}, ~k=1,2\}\) by

Show that \(S\) is adapted to the filtration \(\{\mathcal{F}_0, \mathcal{F}_1, \mathcal{F}_2\}\) constructed in Example «Click Here» .

In financial modeling, stochastic processes are used to describe quantities whose future values are uncertain, such as stock price or interest rates.

Stock Price Model

In this section, we derive a stochastic differential equation (SDE) governing the evolution of a stock price process, whose solution in known as the geometric Brownian motion. We also outline a computational procedure for simulating a stock price process.

Following the motivation from a previous Section «Click Here», let us take the deterministic part of the model as

where \(\tilde{\mu}\), called the drift rate, is the average rate of return of the stock. This model provides a simple description of deterministic exponential price growth. Since stock prices evolve multiplicatively, it is suitable to model the logarithm of the price process rather than the price itself. So, let us consider the process

Then, at the deterministic level, \(X_t\) satisfies the ODE

We now extend the deterministic model by introducing randomness through an additive noise term, leading to the stochastic model

where the term `noise' represents the random fluctuation component to be characterized. Observe that we now use the notation \(\mu\) to denote the drift coefficient, representing the expected rate of change (or mean drift) of the stochastic process \(\{X_t\}\).

The basic idea of a stochastic model is to assume the noise term to be Gaussian white noise. In order to keep the mathematical discussion simple, we begin with a discrete-time approximation of Gaussian white noise.

Consider the partition of \([0,T]\) as

A discrete Gaussian white noise is a stochastic process \(\big\{\epsilon_t~|~t\in \mathbb{T}_n\big\}\) that satisfies the following properties for all \(j, k=0,1,\ldots, n-1\):

- \(\epsilon_{t_k} \sim\mathcal{N}(0,\sigma^{2}_{\epsilon})\), for some constant \(\sigma^{2}_{\epsilon}>0\); and

- the autocorrelation property \( \mathbb{E}[\epsilon_{t_j}\epsilon_{t_k}] = 0,\) for \( j \neq k.\)

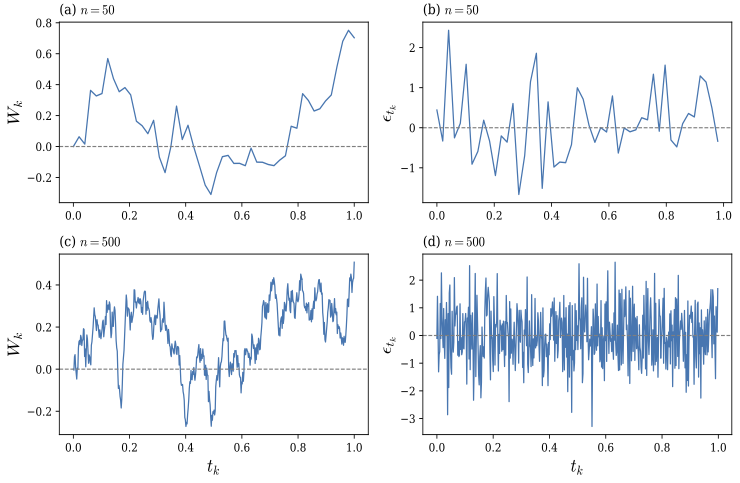

Let us take \(\epsilon_{t_k}\sim\mathcal{N}(0,1)\) and define the discrete process

This process satisfies the recursive relation

with \(W_0=0\), and the process \(\{W_{t_k}~|~k=0,1,\ldots, n\}\) is called a random walk.

The random walk and the corresponding discrete white noise are depicted in Figure «Click Here» for \(T=1\).

Wiener Process

For every \(j,k=0,1,\ldots,n,\) with \(j < k\), we can write

which shows that \(W_k-W_j\) is a normally distributed random variable with

Since \(\{\epsilon_{t_k}\}\) is an independent process, for any \(t_0\le t_{k_1} < t_{k_2} < t_{k_3}\le t_n\), the random variables \(W_{t_{k_2}} - W_{t_{k_1}}\) and \(W_{t_{k_3}} - W_{t_{k_2}}\) are independent because these random variables are sum of two distinct set of \(\epsilon\)'s which are themselves independent.

Now, we consider the limiting behaviour of the discrete-time process \(\{W_k\}\) as the time step \(\Delta t \to 0\). To obtain a continuous-time process on \([0,T]\), we define the piecewise linear interpolation

Thus, \(W^{(n)}(t)\) is a continuous, piecewise linear random function that satisfies (by (2.11), also see Figure «Click Here» (a,c))

By taking \(\Delta t\rightarrow 0\) (or equivalently, \(n \to \infty\)), the sequence of processes \(\{W^{(n)}(t)\}\) converges in distribution (weakly) in the space \(C[0,T]\) of continuous functions to a process \(\{W_t: t \in [0,T]\}\) and we write the expression (2.12) symbolically as

The process \(\{W_t\}\) obtained above is a Wiener process (or Brownian motion) as defined below.

Let \((\Omega, \mathcal{F}, \mathbb{P}, \{\mathcal{F}_t\})\) be a filtered probability space. An adapted stochastic process \(\mathcal{W}=\{W_t~|~t\in [0,T]\}\) defined on this filtered probability space is called a standard Brownian motion (also known as a Wiener process) if it satisfies the following conditions:

- Initial condition: \(W_0 = 0\) (\(\mathbb{P}\)-a.s).

- Continuity property: For each \(s\in \Omega\), the map \(t\longmapsto W_t(s)\) from \([0,T]\) to \(\mathbb{R}\) is continuous. This is to say \(\mathcal{W}\) is a continuous stochastic process (\(\mathbb{P}\)-a.s is sufficient).

- Independent increment property: For any partition \(t_0=0 < t_1 < t_2 < \ldots < t_n=T\), the random variables \(W_{t_1}\), \(W_{t_2}-W_{t_1}\), \(\ldots,\) \(W_{t_n} - W_{t_{n-1}}\) are independent.

- Normal distribution: For each \(s,t\in [0,T]\) with \(s < t\), \(W_t-W_s\sim \mathcal{N}(0,t-s).\)

In view of the above discussions, we propose to take the noise term to be proportional to \(dW_t\). Hence, we write the model (2.10) as

where \(\mu\) and \(\sigma>0\) are constants, and \(\{W_t\}\) is a Wiener process. This is a stochastic model, which is a stochastic differential equation. The process \(X=\{X_t\}\) governed by the above equation is called a generalized Wiener process with drift \(\mu\) and volatility \(\sigma\).

On the other hand, the drift parameter \(\tilde{\mu}\) in the deterministic model (2.9) is interpreted as the expected rate of return (drift) of the stock process \(\{S_t\}\). The corresponding stochastic model for \(\{S_t\}\) is given by

The relation between \(\mu\) and \(\tilde{\mu}\) can be obtained using the Itô's formula (discussed below) and is given by

Therefore, the stock price process \(\{S_t\}\) can also be expressed in terms of \(\tilde{\mu}\) as

which is known as the geometric Brownian motion (GBM).

Itô Formula

As given in Remark «Click Here» , it is important to note that \(\mu=\tilde{\mu}\) holds only in deterministic models. In stochastic models, the presence of randomness alters the relationship between the drift of the price process and that of the log-price process, and hence \(\mu\) and \(\tilde{\mu}\) are generally different. This discrepancy arises because the classical chain rule of calculus is no longer valid for stochastic processes driven by Brownian motion. The appropriate replacement is given by Itô’s formula, which we discuss in this section in a general setting. We begin with the definition of an Itô process.

A stochastic process \(X=\{X_t\}\) is said to be an Itô process if it is governed by a stochastic differential equation of the form

where \(W\) represents a Wiener process, and both the drift and volatility are functions of \(X\) and \(t\).

From Remark «Click Here» , we see that the stock price process \(\{S_t\}\) is an Itô process. Further, we also derived an equation of the form given in the above definition for the process defined by \(X_t = \log(S_t/S_0)\). This shows that the process \(\{X_t\}\) is also an Itô process. The following lemma generalizes this result to any Itô process.

Let \(X\) be an Itô process of the form in Definition «Click Here» and let \(F=F(X,t)\), where \(F\in C^{2,1}(\mathbb{R}^2)\). Then, \(F\) is an Itô process satisfying the equation

where the drift and the volatility processes are given by

Let us take \(F=F(X,t)\), for \((X,t)\in \mathbb{R}^2\) and assume that \(F\) is smooth.

Using Taylor expansion, we can write

Let us consider discrete form of the Itô process

Since \(W\) satisfies the Wiener process, we have

Therefore, we have (dropping the arguments for the sake of notational convenience)

Squaring both sides, we get

Substituting these expressions in (?), we get

Since \(\epsilon \sim \mathcal{N}(0,1),\) we have

Hence, we see that \(\epsilon^2 \Delta t - \Delta t \xrightarrow[]{~\text{m.s.}~} 0,\) as \(\Delta t\rightarrow 0\). This allows us to write

Substituting this in the above expression for \(\Delta F\), neglecting \(o(\Delta t)\) terms and then taking \(\Delta t\rightarrow 0\), we get

for some given \(S_0>0.\) Define the process \(X=\{X_t\}\) by \(X_t = \log(S_t/S_0)\). Show that \(X\) is an Itô process and find its drift and volatility.

Parameter Calibration

In order to simulate the stock price process numerically using GBM given by the formula

we need to estimate the model parameters, namely, the drift \(\tilde{\mu}\) (or equivalently \(\mu= \tilde{\mu} - \tfrac{1}{2}\sigma^2\)) and the volatility \(\sigma>0\). This process of determining the model parameter values from historical data is referred to as parameter calibration.

In this section, we obtain the empirical estimate of \(\mu\), denoted by \(\widehat{\mu}\) and \(\sigma\), denoted by \(\widehat{\sigma}\).

Given stock price observations \(\{S_k~|~k=0,1,\ldots, N\}\) at equally spaced times \(t_k = k\,\Delta t\), define the log-returns

The empirical estimators \(\widehat{\mu}\) of the drift \(\mu\) of the log-return process can be obtained as

The empirical estimate \(\widehat{\sigma}\) of the volatility \(\sigma\) is obtained from the relation

where \(\overline{r}\) denotes the sample mean of \(\{r_k\}\).

The stock price process using the GBM can now be simulated using the formula (2.22) with the estimated drift and volatility, given by

where \(\epsilon_k \sim \mathcal{N}(0,1).\)

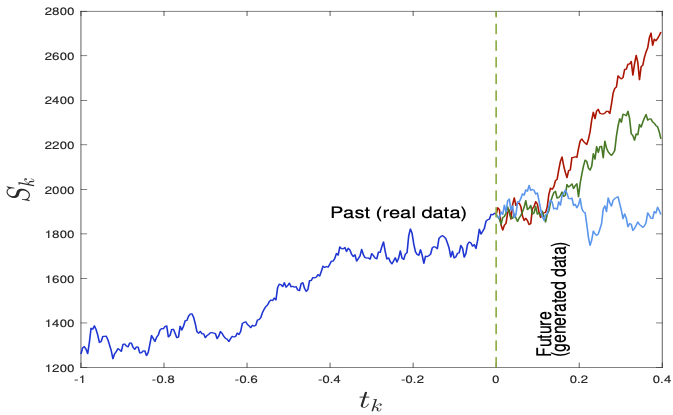

The following figure depicts three sample paths simulated using the calibrated GBM formula (2.23), with \(\Delta t = 1/252\) (a standard convention for the number of trading days per year).

Interest-rate Models

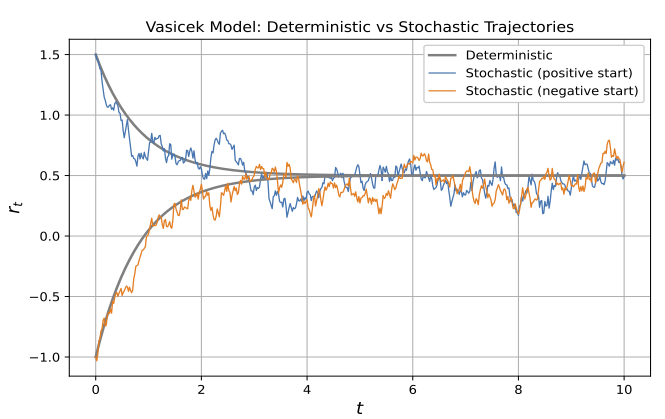

In the previous subsection, we introduced a stochastic model for the stock price process based on a multiplicative growth criterion, leading to exponential behavior in the absence of random fluctuations. In this section, we introduce a stochastic model for the interest-rate process based on the mean-reverting phenomenon, which describes a process that tends to revert toward a long-term average level.

Recall that the deterministic version of the mean-reverting model was introduced in Problem «Click Here» . by including a stochastic component driven by Brownian motion, we obtain the stochastic model for the interest-rate process \(\{r_t\}\) as

where \(\lambda>0\) is the speed of mean reversion, \(\mu\) is the long-term mean level, and \(\sigma\) is the volatility (standard deviation) of random fluctuations.

This model is known as the Vasicek model in the financial context, especially for modeling the short-term interest-rate. Mathematically, the process \(\{r_t\}\) follows an Ornstein--Uhlenbeck process, a Gaussian mean-reverting stochastic process originally introduced in statistical physics.

The Vasicek model (2.24) is a linear SDE, which can be written in the linear form as

Multiplying both sides by the integrating factor \(e^{\lambda t}\) and using Itô lemma, we can rewrite the above equation equivalently as

Integrate both sides from \(0\) to \(t\) gives

Multiplying both sides by \(e^{-\lambda t}\), we obtain the exact solution of the Vasicek (Ornstein--Uhlenbeck) process as

The first two terms represent the deterministic mean-reverting component, while the third term represents the stochastic contribution driven by the Wiener process and is expressed as a stochastic integral, which in this case is a Wiener integral because the integrand is a deterministic function.

Observe that, unlike the stock price process governed by the GBM, the exact solution (2.25) for the process \(\{r_t\}\) cannot be used directly to generate (or plot) simulated data, even when the parameters are given (or calibrated). This is because of the presence of the stochastic integral \(\int_0^t e^{-\lambda(t-s)}\,dW_s\), which is a random variable depending on the entire Brownian path \(\{W_t~|~t\in [0,1]\}\). Thus, the process \(\{r_t\}\) is known only in law (i.e., through its distribution), but not as an explicit function of time.

Wiener Integral

From the above discussion, it is clear that to simulate (or even interpret) the process \(\{r_t\}\), we must first understand how to define and evaluate a Wiener integral.

Let \(\{W_t\}_{t\ge 0}\) be a Wiener process defined on a probability space \((\Omega,\mathcal{F},\mathbb{P})\).

Step 1: Definition for step functions. Let \(f:[0,T]\to\mathbb{R}\) be a step function of the form

where \(a_k\in\mathbb{R}\) are constants. The Wiener integral of \(f\) with respect to \(W_t\) is defined as

Show that for any step function \(f\),

Step 2: Extension to square-integrable functions. Let \(f\in L^2([0,T])\). Consider a uniform partition of \([0,T]\) in the form

Define a sequence of step functions

Let \(f\in L^2([0,T])\) and let \(\{f_n\}\) be a sequence of step functions such that

The Wiener integral of \(f\) with respect to the Wiener process \(\{W_t\}\) is defined as

where the limit is taken in the mean-square sense, that is,

The isometry property of the Wiener integral for step functions can be extended to \(L^2\)-functions.

Let \(\{W_t\}_{t\ge 0}\) be a Wiener process. Show that for any deterministic function \(f\in L^2([0,T])\), the Wiener integral satisfies the isometry property

The above result can be proved easily when the integrand \(f\) is a step function, and this case is left as an exercise. The proof for general \(f\in L^2([0,T])\) is omitted.

Numerical Simulation

We now discuss an exact numerical procedure to simulate the discrete-time mean-reverting process \(\{r_{t_k}\}_{k=0}^N\), for a partition

where \(N>0\) is a given integer.

The Wiener integral in (2.25) at \(t=t_{k+1}\) can be written as

Substituting the above expression in (2.25) gives the exact recursion relation

Distribution of the stochastic increment

The integrand

is deterministic and belongs to \(L^2([t_k,t_{k+1}])\). Hence by Remark «Click Here» , the stochastic integral in (2.29) is a centered Gaussian random variable.

By the isometry property Problem «Click Here» , we have

Therefore,

Exact simulation scheme

Let \(\{Z_k\}_{k=0}^{N-1}\) be independent standard normal random variables, \(Z_k\sim\mathcal{N}(0,1)\). Then, we can write

Substituting into (2.29) yields the exact numerical scheme:

The scheme (2.34) uses the exact transition distribution of the Vasicek model and therefore introduces no discretization bias.

The following figure depicts the numerical simulation of the mean-reverting process using the formula (2.34).